Last year I visited a friend in the US, and he had just bought a house for his family. ”Congratulations on buying a house!” I said. He pointed out to a small closet and replied “oh, that closet is ours, the rest belongs to the bank”. Like the majority of households those days, they would spend the next 25 years buying back their house from the bank.

At this time, I owned two rental properties but was traveling around so I was really homeless, living out of two motorcycle panniers for 6 months. I was starting to feel the need to settle down, and even better, in a paid for home.

Could it be that difficult? Well, yes. First, because prices are higher. Two generations ago, buying a house cash after five years or savings was not unusual. A mortgage would be paid of in ten or twelve years at most. Now we are talking about 25 to 30 years to afford a normal house on a normal salary.

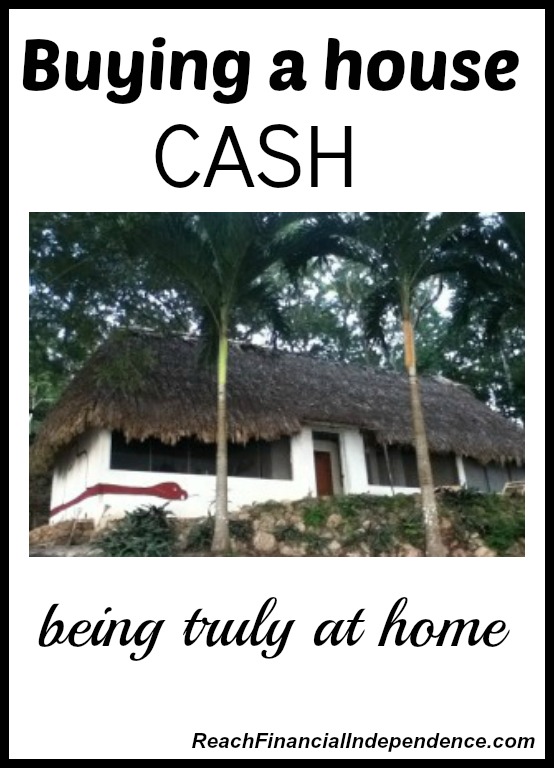

I had to sacrifice a few things in order to acquire a house cash. I chose a country with a low cost of living. I could have afforded a house in France but it would be a ruin in the middle of nowhere and I would have spent the next 5 years fixing it up myself. Here, for as annoyed as I am for having an anthill of workers around my house all day, I don’t have to do the work myself, and they should take three months at most.

Buying a house cash it not always wise.

My mortgage in the UK is at 2.29%. Here in Guatemala, I would have obtained a rate around 8 or 9%, even for a mortgage in US dollars. At 2.29%, I am not repaying my mortgage faster. Like I explained in this post, the average weighted interest rate on my debt load is pretty low, and I would rather have debt and invest my cash than live debt free and have nothing to invest. Of course, down the road, I hope to have no debt and a cash surplus to invest, but for now I need the passive income those investments produce.

I chose to leverage that cash and channel it into several investments instead of using it to pay off debt. As I mentioned, I own some cattle, a coconut farm, a 90 acres piece of land for development, and am considering other unusual investments, but that is for another post. All those things bring me money already, or should start generating an income tomorrow, that is more than the monthly repayment on my debt. If I paid my 2.29% mortgage in full, I would have to borrow the money again to invest, and it would be considered a consumer loan, for which I expect a rate of 7%.

If you have some debt other than your mortgage, killing your mortgage first is probably not financially smart. Your mortgage rate should be your lowest interest debt, and if it isn’t you should look into refinancing because rates have never been so low. You could even borrow more against your mortgage to pay off your higher interest debt. Not to buy more stuff.

But the feeling is truly awesome.

I could have chosen to keep borrowing when I bought my little house in Guatemala. Although as a self employed, semi-retired foreign girl, I had virtually no chance to get an approval on a loan. It already took me four trips to the bank to open a savings account, with no overdraft, no checkbook, no credit line. Just for the privilege of lending them my cash for a 0% or 0.1% interest rate, I didn’t bother reading the fine print. Imagine a mortgage.

But deep down, I wanted to own the roof I live under. That is the first time in my life that I live in a paid for house. I bought my first property at 23 but it was a rental, and I was renting elsewhere for myself. In the UK, I did live in the property I bought, and enjoyed the fact that I had no landlord to tell me how to decorate or abusively keep my deposit at the end of the tenancy, but most of the property belonged to the bank.

As I renovate this house, and build an additional bedroom, I know everything is mine. I never have to pay rent or a mortgage again. I can build more at the pace I can afford to. For now, it is just an extra room, and I hope to have a couple more to run a 4-5 rooms guest house.

That peace of mind is costing me, since I could have invested elsewhere. This is a luxury I deliberately chose to afford. And it is worth every penny.

Do you live in a paid for house? Is it one goal of yours or would you rather use your money for something else?

This post was featured on the Canadian Budget Binder, thank you!

Could not agree more on paying off other debt first Pauline. I’d love to have our house paid off, but it’s our only debt and have other priorities right now. That might change over time, but the rate is low enough that I am not too worried.

investing instead is the smart way to go. if you were bad with money it could be an interesting forced saving.

That’s my goal. I want to eventually retire somewhere, and be able to pay my 50% of cash to buy a home (BF the other half).

I’m not interested in a mortgage, unless the rates are at 2% or way way lower. 🙂

It’s my future goal, but not necessarily one I need to meet now.

I was not particularly in a hurry but I have had a hard time getting rentals since I don’t have a fixed paycheck, sometimes I have had to pay 6 months rent in advance, etc. not having to worry about packing, moving, finding a new place is something I do appreciate.

I own my house and it is an amazing feeling. I know if things ever got to a rock bottom at least my housing costs are pretty much as low as you can get (just utilities, insurance and taxes). It will also make it easier if we decide we want to move. We can just rent out the paid off house and go where we want.

the freedom is really enjoyable! Worst case scenario you can rent for a price under market just to make sure someone keeps the house in good shape, that is a great relief to know you don’t have a mortgage to cover.

Paying off the mortgage is the last thing that I plan on doing. I want to invest my money to earn more and then pay down my mortgage in regular intervals. Yes, I would love to have a house paid for, but it is just not a priority right now.

It really doesn’t make financial sense to most, I am sure you make more elsewhere.

Because my interest rate is miniscule, I’m not at all concerned about paying off my house. However, I am happy to have an equivalent amount that I could use at any time to pay the mortgage, if I choose, in investments.

I had to often teach that concept to clients. It isn’t “paying off the mortgage” as much as it’s “being able to pay off the mortgage when it makes the most financial sense.” That’s what we worked hard to achieve.”\

in the UK I saw some offset mortgage accounts which allowed you to put money into a savings account and not pay interest on your mortgage for the balance of the savings account. You are still free to use the money for anything and start paying interest, I liked the flexibility.

Mortgage rates are at an all time low, as you have said, and if a person can make a better rate of return by putting their money into something else then they should do that versus paying off their mortgage quickly. I know there is a peace of mind that comes with not ever having to make a mortgage or rent payment again too.

With house prices in our city starting at $350,000 and up, I doubt we will ever own a house outright unless we strike oil in our backyard.

time to start digging!

One thing my grandfather could never get over was the fact that the pickup he bought in 1990 cost as much as the house he bought in 1962. Of course, his salary back then was only $100/month, so while he could pay cash for the truck, he couldn’t for the house.

When we had the trailer, we had a 10 year loan but planned on having it paid off in about 8 years. I don’t see myself as a hands-on investor. If we ignore my retirement account, I really can’t fathom myself owning any investments of any kind. So my money will always be put to better use paying debt.

There are still houses you can buy cash in the US, just found one for $650 but you would have to relocate to Flint, MI! http://www.century21.com/property/2102-leith-st-flint-mi-48506-REN007517855

Pauline, you just continue to amaze me with your adventuresome spirit. I love it! We have a mortgage and I’m very comfortable with it. Of course, it will certainly be a joyous day when it’s paid off, but right now it works for us. We still have plenty of money after we pay bills to enjoy a great life.

thank you for your kind words Shannon! most of the time my rent or mortgage was a small part of my budget, like you, although I really like the not owing to anyone. Again, it makes no financial sense and you guys are much better off with a mortgage and investments on the side.

I’d never considered waiting until I had the cash to fully pay for a house, but there are hard and fast rules I have and always will follow: First, always put 20% down. By doing so, we were able to stay above water even during the worst of the mortgage crisis. We never felt completely overwhelmed by our house. Second, go with the lowest term mortgage possible. In both properties which I’ve bought, I started with a 30 year mortgage and re-financed to a 15 year mortgage as soon as I could. Third, plan for your mortgage to be paid off either before your income drops (retirement) or before you anticipate a big cost increase. In our example, our big cost increase down the road would be our kids college, and our recent re-finance would put us having our house paid off before our kids start college. And way before retirement. All of these together will keep us with a mortgage for awhile, but it keeps us in line with our short term goals (build equity) as well as our long term goals.

those are smart rules. My rental mortgage is 30 years but it allows for more positive cash flow and rents should increase over time. For my house, I would go for 10/15 years like you did.

We’re slaves to the bank with our current house. With our next one we do plan on trying to pay it off as quickly as we can.

great goal! it is awesome to see the number shrink as fast as possible.

I would love to own a home one day, but getting a mortage is very difficult! A house in a decent area would cost about 530.000$ and upwards. So now we´re just struggling with saving up the 15% we need to buy something.

ouch, 500K for a home! I decided to move for that reason, I wouldn’t want to have to work for 20 years just to pay for a house in an expensive area.

Originally, I never wanted to own a home outright! It makes no sense because the money is illiquid. I believe in having my money work for me. I downsized 15 years ago to reduce the value of our home. In the 15 years my home has increased a great deal in value. I am paying off my mortgage early only because I will retire in less than 5 years. I want absolutely no debt in retirement.

smart moves. I know it makes no sense to own with low interest mortgages but having no payment allows me to choose longer term investments for the rest of the money, otherwise I would have to keep a lot of cash to cover expenses instead of having money tied up in volatile funds.

Owning a house sounds nice. But there are a lot of caveats.

First, what would I do with all the extra space? Since I live alone, this one bedroom apartment is all that I need.

Second, maintenance. I have no handyman skills and I have no desire to be a contractor. The advantage of apartment living is that if there’s a problem, I just all the office and they send someone to fix it. I might consider owning a condo one day entirely for this reason.

Third, opportunity cost. Where I live, houses are way too expensive for what you get. It’s better to stay a renter and use the money to grow my portfolio of dividend growth stocks.

You make good points, especially about having more space than you need and paying for it on a monthly basis. I have a 3 bed apartment, and used to rent out two rooms when I lived there, now all three are rented. The rents brought a higher return than if I had invested that down payment on the stock market because of leverage. But living with roommates is not for everyone. Re maintenance I have a full time handyman here for $200 to do the garden, small fixes and anything we need, obviously in the US it is more costly and apartment living makes sense. The only thing I don’t like is having little control over HOA fees. My Paris apartment had very high fees usually for nothing.

We plan on paying off our house as soon as our credit card debt is gone. The main reason is that we plan in buying investment properties and I don’t like the idea of having two mortgages.

I know that it might be more effective to use leverage and have two mortgages. My only fear is that if we don’t find someone to rent the property we’d be stuck paying for both houses, which kind of scares me.

I’m really interested in this coconut farm of yours. I think you may have mentioned it before, but not in great detail.

I need to make a post on that, I haven’t yet!

We’re not in a huge hurry to pay off our house since our mortgage interest rate is so low, but we were definitely not keen on owing anything on our investment properties and those will be paid off ASAP.

I have quite a decent breathing room on the rental, so not too worried to pay it off, but if the rental market goes south I think I would accelerate payments in order not to depend too much on tenants to cover it.

I have recently been through this exact decision and I just put my investment property on the market. My husband and I decided it would be best to sell that house and pay off a really huge chunk of the mortgage for our home. We’ll own one home in about 3 years. But no investments. It’s all about what’s right for you and getting the life you want!

exactly, there is no one size fits all. good luck with your projects!

We could never have bought our current house with cash unless we waiting many years. I do hope to pay it off when it is the last remaining debt. I would never stop investing in other avenues to pay off my house, but by putting a bit extra toward the payments, it will be paid off in no more than then years and around 6 if all goes well. At that point, we would have lots of money to invest in stocks or other properties or maybe even bulls if we want!

I get that it doesn’t make financial sense for most. You will have a lot more room for investment once those payments are gone!

We’re paying ours in full in the next couple months once we sort the paper work and move money. We could have invested the money and risk something could happen either we make money or we lose it.. then we still have to pay off the mortgage. At least one thing is for certain and that is the interest rate on the mortgage.. it is what it is.. so we’re going to get rid of it and that leaves us a good 30 years before we retire to keep investing in our portfolio.

I thought you were waiting for the pound to get stronger? check out Oanda fxtransfer if you are looking to change currencies, they have a very tight spread and only charge $20 to do the transfer. Funding the account is free so $20 is all you pay.

I love having my house paid for, of course it is a mobile home so I still pay lot rent. The added benefits are I can move it to land if I want, cut out walls (did that), paint or do whatever I want to it. The lot rent is so much less expensive than actually renting ANYWHERE in this state, that I can put myself through school and will shortly have fully funded IRA’s at the same time. (Full debt payoff is schedule for April 2013). Yes, I could have purchased a bigger house, but why not start small and invest in me instead (school). I am all for doing what makes you feel the most at ease, it doesn’t always have to be the perfect mathematical equation.

Invest in yourself is the most valuable investment you can do, and you are right to do whatever works for you.

Coconut farm huh? Very interesting, can’t wait to learn more about that. We definitely couldn’t have bought our house cash with mortgage prices as high as they are here, but even if we could have we’re more interested in buying an investment property (and hopefully a couple or more someday). Even if the investment property rent just covers the property’s mortgage, the property would be paid in full by the time we retire and then we’d have extra income coming in each month during retirement.

I talked to a businessman who was renting and he said you can only get so much credit, so it is much better to get it for your business than for a house. He is right, although the reasons in my post to own my roof are not making financial sense, I wanted to do it. You are much better off saving for a deposit than paying off your mortgage, strictly financially speaking.

Not only will it be paid for, but you can EARN so much from visitors if you want to. That’s quite an accomplishment!

Yes, the plan is to offset the buying cost by selling parcels and renting the rooms. That would be really cool if the place would end up free in the end.

2 more months/loan payments then it’s mine..my home sweet home, my 1990 29 foot camper travel trailer where I live. YAY !!

whoohoo!! do you still pay a lot rental or own the land as well?

Knowing that you own your only home – really own it – sounds wonderful. There certainly are sacrifices to be made when looking at paying for a home in cash completely, as you pointed out, but at the end of the day you have that satisfaction of not owing anybody.

it is a pretty good feeling!

That’s awesome Pauline. Owning a house outright has got to be a great feeling. You should rename your blog to “HowIreachedfinancialindependence.xxx”

triple x, I am not sure it will attract the right readership!

Sorry, I didnt mean it like that!, I left is as a variable for .com, ,org etc etc :$

Lot rent of 230 a month. 2 miles from the beach. Not too bad.

a real bargain!

I totally agree with your plan, Pauline. We too, the minute our other debt is gone, are going full board on paying the house off. Can’t wait to experience that wonderful feeling!

I hope you can soon, it is really amazing.

I am so impressed with your diverse investments. You are doing exactly what I plan to do once I am debt free and 2.29% mortgage rate is awesome. Can’t wait to see what happens with your 90 acres!

thank you! 2.29% is UK, I don’t recall someone having such a low rate in the US.

This post was a treat to read! I’m planning on owning rental properties in the future, as well. But it was interesting to read about your different options in other countries. I plan on sticking around the US, and my first property will be either a duplex or a triplex, so I’ll have a ‘free’ place to live while starting to collect rent checks at the same time.

thank you Sharon! That sounds like a great idea, having people cover your mortgage and being on site at the same time. My UK property has been blissful to manage but if something bad happens, being an ocean away, there is not much I can do.

Reducing the mortgage would be the last thing which I plan on carrying out. I want to speculate my money to help earn more than pay down our mortgage in regular intervals. Yes, I would like to have a house covered, but it just isn’t a priority today.

Looking Forward to Another Great article. Good luck to the Author! All the best.

I bought a townhouse last April and paid $60k cash in the US near Washington, DC. The house has tenants in it paying rent and I should make back my investment in about 5-6 years. I saved that money living rent free with my parents (they have no mortgage either). I’m mid thirties and while my friend bought a $400k townhouse and is struggling, I choose to do something different because I’m working my $80k government job for 17 more years then will retire with a paid for house or two.

I’m just an everyday girl that likes to sleep and not worry about bills and debt. So I made different choices from everyone around me and they are paying off literally.

Purchasing a house is extremely astounded process since we will spend our entire saving money on our fantasy house so on that time I think one thing is rotated in our psyche. We spend our cash in the correct path and for better house. Once in a while in view of the absence of learning about property we burn through cash just for house yet overlook this principle where and which zone is house found.

Owning a house outright has got to be a great feeling. That’s awesome Pauline.

A new home is naturally appealing and gives potential renters the comfort of knowing the house is in its best possible condition from the start. It also minimises maintenance problems, saving you the money and time needed to deal with them.