This is a guest post by seventeen year old Eva Baker, founder of TeensGotCents.

Eva

Eva Baker is a high school student passionate about preparing for her financial future and helping other teenagers prepare as well. When she isn’t rock climbing at the gym or pinning ideas for her non-existent wedding, she documents her financial journey over at TeensGotCents.com. Find her on Facebook, Pinterest and Google+!

Eva Baker is a high school student passionate about preparing for her financial future and helping other teenagers prepare as well. When she isn’t rock climbing at the gym or pinning ideas for her non-existent wedding, she documents her financial journey over at TeensGotCents.com. Find her on Facebook, Pinterest and Google+!

There are so many things to buy. So. Many. Things. As a seventeen year old in a culture saturated with commercials and advertisements I am well aware of the latest and greatest things that I absolutely must have now. But wait. I don’t have to be an adult to see where that road has taken many people. I hear about families that have $70,000.00 in credit card debt on top of their student loans. College graduates with great jobs that can’t buy a home because of the debt they have accumulated. This is not the road I want to travel. My plans involved no credit card debt, no student loan debt and living within my means. I don’t have plans to be super rich or to travel the world. I just want to be free. Free to help others in need, free to give to worthy organizations, free to pay my bills on time and eventually take the grand kids to Disney regularly (and pay cash for everything)! That kind of freedom simply does not exist when you are buried under a mountain of debt. So, here’s the plan:

There are so many things to buy. So. Many. Things. As a seventeen year old in a culture saturated with commercials and advertisements I am well aware of the latest and greatest things that I absolutely must have now. But wait. I don’t have to be an adult to see where that road has taken many people. I hear about families that have $70,000.00 in credit card debt on top of their student loans. College graduates with great jobs that can’t buy a home because of the debt they have accumulated. This is not the road I want to travel. My plans involved no credit card debt, no student loan debt and living within my means. I don’t have plans to be super rich or to travel the world. I just want to be free. Free to help others in need, free to give to worthy organizations, free to pay my bills on time and eventually take the grand kids to Disney regularly (and pay cash for everything)! That kind of freedom simply does not exist when you are buried under a mountain of debt. So, here’s the plan:

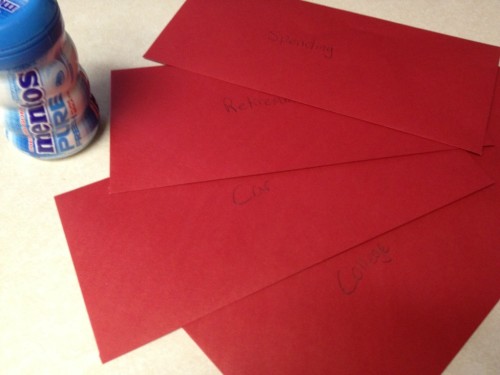

The envelope system.

I use the envelope system as a way to help myself make good financial choices. Something about spending cash helps me to make better decisions than sliding my debit card. It also helps me to direct where each and every dollar goes. I have to make a purposeful choice when I put my money into an envelope. I plan to use a cash system long term in order to keep up the self control that I need to be successful in my financial goals.

These are my envelopes…

Emergency Fund.

In 2012 I was determined (after listening to The Total Money Makeover by Dave Ramsey) to save up my first $1,000.00 as an emergency fund. It took me almost the whole year but I did it! The emergency fund makes sense. Things break and accidents happen. If you have no savings whatsoever for this then you will probably end up using a credit card. Which is only a good idea if you want to pay for that new outfit for the next 16 years.

No credit card.

If I don’t have one I can’t go into debt with one. I have read advice on keeping one for emergencies and I suppose that could be wise. But it needs to stay at home at the bottom of a drawer so that you never actually use it. Or see it. Depending on your personality it may be best to not have one at all.

You know what these are for…

No student loans. Ever.

I have committed to going to school without incurring any debt. If it takes me longer than the normal amount of time to finish school, then so be it. NO. STUDENT. LOANS. I know that such black and white thinking may seem immature on my part, but I believe that this will serve me best in the long run.

Save for retirement.

Saving 15% of my income is also a long term priority. If I start saving now it is amazing to see how that money grows over the course of a lifetime! It’s pretty exciting! I realize that I may not be able to save when I am in college because of the expense, but I can save now. I currently have $30 in my retirement envelope and I hope to have a lot more by the end of the year! That doesn’t seem like much, but over the next 50 years it’s gonna make a huge difference!

Don’t marry an idiot.

That really is self explanatory isn’t it? But the truth is that I can’t marry someone who refuses to be wise and disciplined with our finances. Obviously, there are all sorts of other things that I will be looking for in a husband, but this is one key issue for me. I’m not killing myself now just so I can marry someone who wants to spend everything we make and get us into debt. No thank you…

Sometimes I wonder if I will look back on the things that I am writing now and chuckle at my lack of sophistication. Maybe I will. But I don’t think that will be the case. And if I don’t follow through with this and have credit card debt and student loan debt and all of those other problems….well, 17 year old me is gonna punch 30 year old me right in the face!

be centsible!

Editor’s note: How awesome is that? A 17 year old with a retirement saving envelope?? Congratulations Eva, you are definitely on the right track to financial freedom!

The only thing I disagree with is not taking student loans even if that means staying at school longer. Studying has a cost, room, board, etc.. and since you should make more once you graduate than as a student job, it can make sense to borrow for your education. Not for parties and beers obviously.

Since you are dual enrolling and taking free college credits I have no doubts you won’t need the loans anyway. Thank you for sharing!

This post was featured on Norwegian Girl, The Heavy Purse, Monster Piggy Bank, The Frugal Farmer, Canadian Budget Binder, Frugal Rules, Think Rich Be Free, THANK YOU!

that`s the right attitude, Eva! I wish I had been just as wise as you when I was 17.. I`ve always been good at saving, but I never thought long term about money when I was at your age.. Keep up the good work:-)

Thanks so much! I just added $20 to my retirement envelope. It is a little hard to get excited about 50 bucks – but it’s a start!

Wow, wow, wow! Way to go Eva.

Thanks!

It is people like you Eva that give me hope for the next generation. Where were the women like you when I was 17? None of the girls I knew at that age cared about their finances or the future at all.

Thanks so much Glen. Seeing my mom and so many family friends face tough financial times has really made me more aware of how important it is to plan for the future.

Great attitude. The only thing I’d recommend is to make those envelopes electronic, except maybe for your spending money. Then your retirement, college, and car money becomes “out of sight out of mind”, and you won’t be tempted to dip into them,

That is a good idea. I am just getting started and placing the cash in envelopes feels good to me – but my mom uses EEBA and I may move to that sometime soon because there is a free version. Thank you!

I’m impressed with how much you care about personal finances at 17! I also agree with Pauline’s advice that taking out student loans might be a good choice if it means finishing college on time. It’s not unrealistic for your income to double when you graduate, which can really help you pay down those loans and start saving and reaching other personal finance (and life) goals.

This is something I may change my mind on – never say never – but seeing friends go through such tough times because of debt when they unexpectedly lose a job makes me really cautious. Thank you for leaving a comment!

Brilliant article Eva, it’s great to see you’re taking such a sensible approach to money at a young age. And buy the time you’re 30 I’m sure you will be thanking your 17 year-old self, not punching it in the face!

Thanks Ashley! 🙂

Generally you seem to be on the right track. I do think that your fear of credit cards is a bit irrational. You would be wise to start building some credit history. Even if it means is that you use your credit card to pay the cable bill, or the car insurance bill, you’ll at least be building up a history of paying your bills on time. This will help if you ever need to get a mortgage down the road.

I would also not worry about student loans. A much better question is what are your post education job prospects. If you take out loans to become a cardiologist, you’ve made a good choice. If you take out loans to study dead languages and wind up bagging groceries because there’s no employment for you, then that’s a bad choice.

I agree with you about getting a degree in something worthwhile – my mom and I call those ‘other’ degrees the ‘Do you want fries with that?’ degree. (That isn’t very nice is it?) Definitely not what I am going for!

Wow, what a great attitude Eva! I love that you’re taking such a wise and balanced approach to money. This is something that so many people should read. While I may not whole heartedly agree with your stance on student loans & college I greatly admire your desire to stay out of debt. Debt seems to be so easy for many to take on that it’s so refreshing to read posts like this.

Thank you John. It’s a little scary to have people disagree with you on the internet and I know that I may change my mind on some issues as I get older. Thanks for the encouragement!

Very inspiring indeed at young as that. You are already aware and motivated to strive all the best for your financial future. Yo are in the right mind set, wish you good luck.

Thank you!

Wow Eva, it sounds like you know more about money than 99% of adults, but I’ve got 2 nuggets of 24 yr old wisdom for you. 1) I wish I had a credit card at your age just to build credit. The only thing hurting my credit score is length if credit history. (You might want a mortgage some day).

2) you’re always going to laugh at what younger you wrote, even if it was only a few months ago. Good luck!

Can seventeen year old’s get a credit card? I never even thought to ask! And you know – the worst thing about having a blog is that I get to have a permanent record of everything I ever thought about on personal finance on the web for everyone to see…(nervous laugh)…

I think you can get a card but it would have to be under your parents’ name and I am not sure that counts as credit building. I do second the thoughts however that it is good to build a (n impeccable) credit history even if you only pay a $5 monthly bill with your card.

Oh, right. It looks like you have to be 18 to get a credit card, but I’m sure that will happen soon enough. Yea, I prefer to stay anonymous partly because I don’t want that permanent record of my silly rambling out there, haha.

Yeah. I may regret the whole ‘let’s tell everyone who I am’ strategy in the end huh?!? 🙂

The don’t marry an idiot one should be on there eve if you have a lot of money! Those are some really good rules to follow. One thing I would encourage people to consider though is that taking out student loans is necessarily a bad thing. If you think of it as an investment in your future, it can be well worth any money you spend. The key is to not take out too much, and to stay disciplined about paying it off.

So true Ryan! I agree that having a plan to pay off debt is really important – thank you for leaving a comment!

Wow you are awesome! Sounds like you are on a great track.

Thanks Michelle!

Are you SURE you don’t want to be adopted? 🙂 What a great strategy.

Keep at it!

My mom said that I’m not available! 🙂 Thanks William!

Good for you Eva. It’s amazing that you already are aware of what you should do, how to handle your finances, and that you have already set your goals. Keep it up.

Thank you! I have my parents to thank because they took the time to help me learn these things.

Glad to see that some youth have their head on straight. This type of thinking will take you very far in life and will prepare you for life’s little hiccups. Good luck to Eva.

Thank you Grayson!

You should have a credit card, and you should use it. Just don’t put on more than you will pay off in a month. Building credit early will be important when you need a loan for your first car, or when you need to rent your first apartment!

I haven’t thought about needing credit to rent an apartment. I’m planning to live at home for college because of the savings, but eventually I will have to think about building credit. Thanks Jenny!

Your credit score will even affect your car insurance rates! It’s crazy.

The smart thing to do at this point in your life is to charge everything BUT move money from your budget envelope to a “spent” envelope to cover the cost immediately. Then, the day your statement is available, deposit the “spent” money back in your account and pay the bill online. That way, you don’t have the temptation to go into debt.

Choose a high-rewards card, and you’ll get a tiny bit back, too.

Wow! I love your attitude and you’re displaying far greater financial savvy than most adults! You’ve got a bright future ahead of you, Eva. Because establishing excellent credit is important for future home loans, I would encourage you to adjust your stance on credit cards slightly. They can absolutely make it too easy for people to go into debt. But when used properly, they can be a great tool to establish good credit. Just always buy what you can afford and pay your bill in full every month.

Very good points Shannon – thank you so much for leaving a comment!

Great Job EVA, I hope my daughter can be as focused as you at such a young age. You will do just fine with your finances, I am sure of it. Excellent post and great blog you have!!

Thanks Jim!

What a very mature and intelligent 17 year old! If only I could have been as smart when I was 17! Here’s to hoping my daughter will be as responsible as you!

Thank you Nick – I’m sure that she will with your help!

great ideas, eva! the envelope system works. i’ve seen it in action and wholeheartedly endorse it. we have that whole student loan thing looming large in our lives right now – still debating on that one, but have to make a decision any day now – so thank you for your input.

my favorite part was “don’t marry an idiot” and that photo of the scissors. really great points all by themselves!

I wondered if anyone noticed those scissors! Thank you for commenting!

Nice article, Eva! Yes, you might look back in a decade and see a lack of nuance, but I think it’s better to be extreme and principled when you are young than regret being the opposite later on. I also was afraid of credit cards for a long time, but I trained and learned that I could trust myself and I still have a record of perfect use. You will figure out what’s best for you and you’re off to a great start!

Thanks so much Emily. Seeing how credit cards are abused just makes me want to avoid them completely!

Hang in there Eva! It is completely possible to graduate without student loans. I am just finishing my sophomore year with no debt. I will not be taking any loans to finish my undergraduate degree. My brother was able to attend a private college for the entirety of his bachelors without taking any loans. He is now being crippled (along with many people I know) with law school debt. Considering the economy, there are very few (if any) bachelors degrees that guarantee you a job and if a masters program is necessary, having debt from your bachelors won’t be helpful.

Wow. That’s something that I haven’t thought about Rebekah. Student loan debt for a bachelors and grad school? Ughhhh… I’m so glad you brought that up. Thanks for the comment!

Great plans. I was so thinking about buying clothes and a car at 17 and had no idea about debt or how to stay out of it. Credit cards and student loans can be good if you use them to your benefit and don’t take longer than necessary to pay them off. I’m sure you’ll make wise decisions. It sounds like you have a very good grasp of finances. Keep up the good work.

I will admit to doing a great deal of thinking about clothes and accessories. And lip gloss…and shoes!

Wow! If only more 17 year olds thought like you. I’m sure you’ve heard this several times already from people older than you…but it’s true. If I only knew what you know when I was your age! You’re DEFINITELY on the right track! Keep it up!

And as several other commenters have mentioned, credit cards are good if you know how to use them correctly. If you PAY OFF THE BILL IN FULL when it arrives, then you’re ok! You’re creating a good credit history. Plus, at some point you’re going to want to rent a car, a hotel, book a flight, etc.. and you’ll need a credit card.

Formal education is good if you plan on getting a job and working 9-5 for someone else. But if you want to become an entrepreneur, there are hundreds of examples of successful business men and women who run mulit-million dollar businesses without a formal education. So I guess it depends what path you want to go down.

I heard Dave Ramsey say before something like “don’t get a student loan for a degree that your salary can’t pay off in one year” (something along those lines) So if you plan on getting a degree that will land you a job with a salary of only $24k/yr but your student debt is $48k…then that’s a bad decision. But if your student debt is $24k and your degree can get you a job with a salary of $50k…then you’re ok.

Wishing you much continued success with your blog and your finances!!

P.S

What got you so interested in money at such a young age? And what kept your interest?

I’m looking for ways to teach my young daughter and get her interested..

Couple of things got me interested in budgeting and personal finance. My parents taught me to be careful with my money from a very young age by giving me an allowance. We also had many family friends lose jobs/homes/everything because of the economy. Listening to the Dave Ramsey book came at a really important time as my parents were getting a divorce and I saw my mom starting over and following Dave’s ‘babysteps’ herself. I think all of that combined made me think a lot about how I wanted to handle my money.

Bravo for going against the grain. You’ve learned at 17, what many adults will never learn. I suppose some good has come out of the financial irresponsibility of others. Great job!

Thanks so much Justin!

Well done mate! At 17 I am going to say my mind was in the same place as yours. I didn’t have Dave Ramsey to guide me nor did I have the internet to read blog posts but I did see what was happening around me. I noticed what happened at my mates houses and I watched the tele and read the paper. Not all young people think like you do and if you continue with your goals you WILL get to where you need to go. I also had no student debt when I went to University as I saved to pay cash and then went on to buy my first home at 21 . Cheers!

That’s part of what got me interested in managing my money well – seeing others really struggle financially in these last years. Thank you!

My two cents worth (at 27).

Get a credit card – if you’re a disciplined person. I got my first younger than you (as a signatory on my parents card, as I lived away from home, and it was for emergencies). I paid any debts to them should I have used it between pays etc. Then I got my own. I always pay it off. With that in mind, I don’t go nuts.

Student loans – US loans are insane – I find it hard to work out how ‘lucky’ the US is in comparison to sunny Australia (where we pay 25% of our education costs, the govt the rest, and our 25% can be offset til we’re earning)! So you’re call. But I’m an engineer, with a great paying job, so the ‘debt’ was worth it – and I didn’t pay all of mine up front every semester, but most. BUT, which it’s a ‘real’ degree and job, I know Americans who’ve found it harder to get a job nonetheless

Retirement – I already have $60k in retirement – but not in an envelope. Look into what ‘retirement’ funds exist. Again, in Aust, we have ‘super’ and it’s sole purpose is for retirement, you CAN’T touch the money, and every employer is made to contribute 9% by law to it. (It’s going up to 12% in the next few years). So even student jobs pay super. Maybe make a rule with yourself that you’ll put 10% to retirement every pay? The compound interest is well worth it. I personally chose to add $50 per week above my company’s generous 11% (they are doing more than the current law). I can afford it now, and when I take time to have kids, I will be thankful.

Partner – don’t underestimate a partner you might need to lead into better finance management. Not every person learns or thinks on these issues, but they might with exposure. Rest assured, different money personalities can work in a marriage (ie my spend-y mum and my frugal dad) – they teach each other lessons in restraint, but also when to enjoy and let loose – and balance is crucial!

60K in retirement already! You are my hero! If I didn’t hate math so much I would seriously consider becoming an engineer myself! 🙂 Thank you for sharing your thoughts with me – very helpful.

What a wonderful plan you have, Eva! You are an inspiration to teens everywhere!

That is so nice of you Laurie. Thank you!

I think it’s more important to make sure you know what you want to do with your life and your potential degree before starting college than worrying about loans. If you pick the right career (that’s right for you, not necessarily one of from those “most in demand/highest paying” lists that circulate), then you will pay those loans off pretty quickly. But the wrong degree and you are just wasting your money, whether you borrowed it, saved it, or earned it.

I agree completely. I am pursuing a specific career path that requires a two year degree and that will allow the flexibility in work hours that is important to me. I also think that it is important to set specific goals – like not taking on student loans – so that you don’t lose your way financially during the college years.

Eva, you are wise beyond your years! I am proud to know you!

Thank you so much!

For someone your age, you have a very good outlook regarding finances. Your suggestions regarding emergency funds and envelope system are truly amazing. The use of credit cards for emergencies is also a practical option.Other young people should really follow your example.

Thank you David. I’m really proud of my emergency fund but I know that I have a long way to go!

Eva you are on the road to great financial freedom. I disagree with the editor’s note, because I have been taking on school as I can pay for it too. I don’t see the point to student loans, even if it takes me longer to finish school. Maybe it has to do with me never wanting to be in debt again, but I don’t know if I want any loan.

I get the point of not wanting any loans, but this is like the debt snowball example. Paying off the smallest debt first is great for momentum, and getting started, however, it makes more sense to pay the highest interest first. In the case of student loans, if you can get a decent job and salary once you graduate, you will make the tuition money back in less time than if you have a basic job and pay for college as you go.

I guess it all depends on what sort of job she can get once out of school. I have seen way too many friends take jobs they hate, just so they can pay bills. Eva is strong and courageous for not taking on any debt, even the so-called good debt of student loans, but I wouldn’t want her to take on student loans just because others say they are good. I think she should keep doing what she is comfortable with, because it seems to me that she is way ahead of the rest of us. 🙂

Wow, this is such a very wise kid. Surely, she will have a great and promising future ahead if she will continue to do this saving thing and she is definitely right about credit card, never to have one to really avoid yourself from getting a mountain of debt.

Eva this is really helpful and interesting post. I really like and agree with your “Don’t marry an idiot” and having an”emergency fund” points most. Thanks for such post. And I am struggling with some of these issues. Anyway thanks!

Thank you!

Always interesting to hear a teenager’s take on finances and technology. Good stuff.