Today’s post comes from Alex. He blogs over at Mutilate The Mortgage and is giving away a few free gifts just for Reach Financial Independence readers. Head over to www.MutilateTheMortgage.com to find out how to pay off your mortgage in under 10 years! Let me know if you would like to guest post on RFI.

So last year DW and I flew to Fiji and relaxed on this very beach. We were completely alone. All day just us and the Sun. The peaceful lapping of the water and the soft, warm sand between our toes. It was relaxing and entertaining all at the same time.

Relaxing because… well, come on, just look at that scenery!! But entertaining also as it was just so beautiful to look at and watch pass by, like watching one of those nature demonstration video’s they play at TV shops on the huge 199″ TV’s… except this was in real life.

I’m sure at some point you’ve dreamt of retiring to live and relax in this type of environment but that’s only for the privileged. The rock stars, the billionaire Facebook entrepreneurs and those born into wealth. For you and I it’s the beige cubicle prison for 40-50 years then MAYBE a bit of golf before we die and that’s if we’re “lucky”!

But I’d like to show you that there’s a new path now. One that requires a fraction of the work and that gets substantially better results too. How? It’s partly to do with planning but also a lot to do with simply living in the future.

The Current Path

It’s not hard to learn about the current path to retirement. Most people will gladly tell you what you should do (which will be exactly what they’re doing of course) and it usually goes along the lines of: go to school, go to uni, get a good job, repeat boring job ad nauseam for 50 years and then retire to be old, play golf and then be admitted to a retirement home and hope that you saved enough to actually pay for it all somehow.

I don’t know about you, but considering the calibre of most of the jobs I’ve seen and done working them for 50 years sounds like hell.

This is what we get told by our parents, by our bosses, by careers counsellors as it’s what’s been done in the past. As a side note I don’t think there’s anything I hate hearing more than “we do it that way because that’s how we’ve always done it“. Makes me want to smack my head against a brick wall ughh!!

So while every person will happily agree with each other that things have definitely changed since the 1950’s, they also for some reason think that this career path is still the best way to go.

So What’s Changed?

Put simply, it’s our productivity. We’re FAR more productive now than we were even 10 years ago. In 1960 you would physically travel to the library, look up book categories in a card catalogue system and then go physically find that book, spend even longer swiping through the pages to find what you were looking for, finally hitting upon the answer you were after – that the current population of Russia is 120 million.

Contrast that with today where you can literally not even move a muscle and just yell at Siri and have her tell you the answer in 5 seconds. My kind of world 😀

Productivity has made huge strides in all fields, building upon itself over and over making almost everything better in every way. The $50 smartphones you can buy in Target are billions of times more powerful than anything 50 years ago and these enhancements mean that today’s life is considerably cheaper and easier. The cars are faster, cheaper to buy and own even though they have tons more features and power. Through genetic modifications, automation and new farming processes we’ve made food more abundant, cheaper and of a higher quality too. We work far less to produce far more even when you take into account inflation.

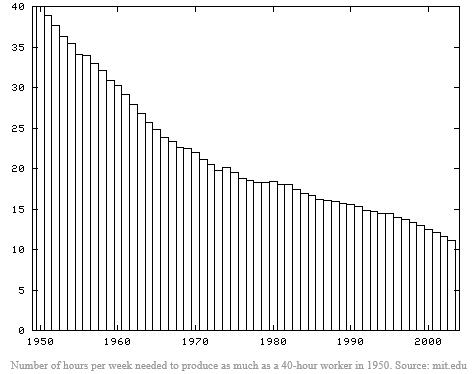

In fact, studies have shown that productivity has increased SO much that “an average worker needs to work a mere 11 hours per week to produce as much as one working 40 hours per week in 1950”. 11 hours. Unfortunately most people continue to work the full 5 days a week and just spend that extra income on random life luxuries because the idea of working for 40-50 years is so ingrained in their mind. This is why there are now extremely ludicrous infomercial products like the Wearable Towel, Shake Weight or the totally awesome and amazing Rejuvenique Electric Facial Mask (go on, Google that last one, I dare you!).

Number of hours per week needed to produce as much as a 40-hour worker in 1950. Source: mit.edu

The New Path

There is a different way to handle it though, which is to still work that full 5 days a week… but only do it for one fifth of the total time. So instead of your 9-5 job for 40 or 50 years you get a 9-5 job that only lasts 8-10 years. This allows you to take any “normal” job you’d like, full time and yet still execute an overall plan that’s vastly different to almost everyone else out there.

In those 10 years you still live a good, healthy life but you save that extra 65-80% income, invest it wisely using the newer, cheaper and better financial tools available now and then retire after your stint is up. It might sound strange hearing that you can easily live on 20% of your income but there are people all over the world doing this right now, Mr. Money Mustache and Early Retirement Extreme are two very high profile examples of this.

A few decades ago this wasn’t really possible as the efficiency improvements just weren’t there but today, together with financial tools that are cheaply and easily available to everyone, all the puzzle pieces are firmly in place. It’s just taking time for more and more people to catch on to this reality that your working life doesn’t have to last 50 years any more if you make the right choices.

How To Use The New Path

Now it’s all well and good to point to some dude on the interwebs and say “there you go, he did it so you can to” and end my piece there. But showing is always better than telling so I’d like to outline a brief example of how this new path might work.

Firstly I’ll state that this new path isn’t a complete get out of jail free card. You can’t just ditch school in year 10, watch TV all your life and expect to be retired and a millionaire by the time you’re 26. The first parts of the “old plan” actually still apply quite well today, the parts that say go to school, go to uni and get a good job. This is the initial key that allows you to start earning a consistent and substantial wage throughout your life and that’s critical. What happens after you get that job though is where things diverge.

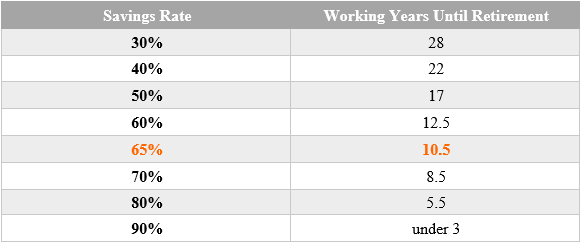

Finances can get complicated quite quickly and although I don’t know anything about your personal finances you can easily reduce it all down to one number – your savings rate.

Savings Rate = [Money Left Over After Expenses] / [Total After Tax Income]

It’s usually calculated on a yearly basis so for example you might earn $60,000 a year after tax as a software engineer. You live your life, buy food, power, phones etc and end up spending $25,000 for the year. That means your savings rate is just:

Savings Rate = ($60,000 – $25,000) / $60,000 = $35,000 / $60,000 = 58%

Not bad. That’ll have you being able to retire in around 13 years. Doing this calculation for a range of values you can see how the different percentages vary:

As you can see, at 80% savings rate (probably quite near the maximum I’ve seen anyone get to) your career length is only 5 years! If you’re not that extreme though you can pick and choose your length, adjusting it to your abilities and your goals. Personally we’re aiming for anywhere in the 8-10 year mark and so far we’re bang on track too.

Beyond the above general “plan” there are two other core components that make this work:

- Being able to live off 25% of your wage

- Being able to properly invest the remaining 75%

The first one is mostly a decision made by you. How much is your time in this world worth versus the general “stuff” you would like to buy. Is having a sweet new car every 3 years’ worth working another 10 years? What about cable? Two cars versus one? A new phone every year versus every 2-3 years? A huge flashy house versus a modest 2-3 bedroom one? How much are you happy to do without given how much it will reduce your working career? The challenge is mostly in the mind.

You might react to me saying “live off 35% of your salary” by scoffing or assuming I have no idea what I’m talking about but the fact remains it is possible, it’s simply a matter of you choosing to live a more simple life in return for huge rewards later on. We have and currently live off about 28% of our income. I’d also say we don’t really live hard lives either however I do admit that as your income increases it becomes easier to live off lower and lower a percentage. This is why the first part about getting a good job is still important.

The second point above is usually a journey that you have to embark on yourself. It can take time to properly research, understand and fully flesh out all the various asset classes, investing methods, reasons, research, stats and also define what it is that’s important to you about investing but you need to know the research, know the why of what you are doing.

Maybe you’re an extremely safe investor or not as young as most and so need a higher bonds to stock ratio. Maybe you are fantastic at building and repairing houses and so choose to invest heavily in real estate. Whichever way you go it’s important that the extra money you’re saving does indeed go towards retirement savings.

Your Results

It takes time, patience and discipline but your results will quickly become evident. Money will begin to flow in, build up more and more until you’re racing along to that final date.

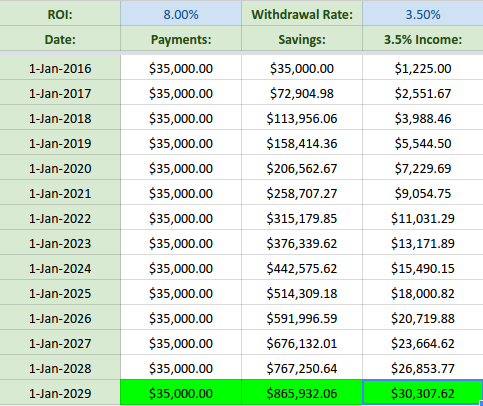

As you can see below in a simple use case, when saving $35,000 a year similar to the savings rate of 58% above, things build up very quickly over time. After 13 years of doing this and assuming you get no pay rises (which is usually unlikely) and a return of around 8% then your savings sky rocket to over $800,000 allowing you to withdraw a highly conservative $30,307 or 3.5% each year. This would easily cover the $25,000 expenses and still enable your investments to continue to hold their own against inflation and likely even continue to grow.

Although this might seem rather simplistic in nature take note that this plan doesn’t rely much, if any, on external sources. There’s no “win the lottery” or “get $1mil in inheritance” in there. It works for virtually any income level and even if you don’t have a yearly return of ~8% on your investments as used above, this doesn’t substantially affect your results. This is because you balance grows so quickly over such a short period of time the effects of compounding returns doesn’t have much time to make a difference.

Working no longer has to be a 50 year cubicle sentence. With today’s advanced financial tools you have easy access to powerful investment options that were impossible even 20 years ago. That together with the huge and ever increasing efficiency improvements of the last 50 odd years have opened up a different path for you to choose.

Follow it and then retire like a boss!

You got it spot on regarding productivity. Thanks to the Internet And technology life is so much easier now.

Sam

Increasing your personal savings rate is a powerful tool. Not only will it help you reach financial independence more quickly, but it enables you to live on less, as well. It helped my father retire by 62, and I hope to apply those same tactics.

It is indeed a doubly powerful tool, allowing you to save more AND reducing the amount of money you have to save up by a factor of about 30. It’s usually also ends up being better for your health and the environment too ☺

Spot on. Although having shared this article with a few friends, they criticized the “8%” value which they called unrealistic. Sadly this kind of ruined the article for them. I think they were reading the whole thing looking for what was “the catch”, and they decided it was the 8% number. I think 8% is fairly optimistic, 6 or 7 might have been easier for me to “justify” to them.

Other than that, great article 🙂

Yay! Ten years and retire like a boss. It seems really achievable! With the right decisions and timing.

I just got serious about early retirement a month or so ago. Planning on cutting expenses, downsizing and investing whatever is left. The only thing is pumping more and more money into equities when the market is already in record highs. It is scary. I am not sure about 8% return either. Seems like I need a little bit more encouragement from the early retirement community. 😊

Great line of reasoning. As important for the new path is ensuring you’re paid at a similar portion of your productivity as your grandparents. This can be tricky with reduction of unions, but you can counter by seeking a job in a more competitive market sector.

So here is my dilemma – do I count 401(k) savings? I would argue this is the most long-term saving I am doing for retirement, but it’s pre-tax income and according to your formula shouldn’t be included…

Yes, you should include your 401(k) savings because that is money you’re saving. Generally, a paycheck looks like the following:

GROSS PAY – PRETAX SAVINGS – TAXES = NET PAY

The miscommunication probably comes from how we usually read “Total After Tax Income”. Even when I read that, the first thing I think is that it is referring to the amount of money from my paycheck that gets deposited in my bank account (which is really net pay). Then I have to catch myself because it’s really referring to the total amount of income I get, minus taxes.

In other words… TOTAL AFTER TAX INCOME = GROSS PAY – TAXES.

And in general, another way to look at is is TOTAL AFTER TAX INCOME = NET PAY + PRETAX SAVINGS.

Hope this helps!

Great explanation of the FIRE process! Unfortunately for us, we have to follow a somewhat different path because of our debt. I will definitely not be a full-time worker for decades to come, but we are designing a unique path that involves some flexible, part-time. The low income will be enough to cover low, debt-free living expenses while our investments can grow without unhindered by any withdraws.

However you do it, there important thing to keep in mind is that there are other options. And you’ve done a wonderful job illustrating why we need to set our goals higher than working till we play golf and move into a retirement home.

I agree with the general idea of this post, but I have a few thoughts:

You imply that our dramatically increased productivity has brought with it an equally dramatic increase in income. I don’t think that’s correct. Employers now expect higher productivity, and wages are at historic lows according to most sources. I don’t think productivity has anything to do with being able to retire early. It is much more dependent on keeping your expenses low and your savings rate high, which was discussed. I think this strategy has been possible for a very long time, even before Siri was around to help.

You also make it sound easy to live on a very small percentage of your income. This is not the case for most people, especially those of us who live in high-cost areas like Los Angeles, San Francisco, New York, etc. Paying rent, not to mention an average mortgage, will consume a disturbingly large percentage of most people’s salaries. You also don’t mention taxes, which can easily wipe out 20% or more of one’s salary (especially if you’re not maxing out your 401k in order to save up for a down payment on a house).

It is easy to save a lot more than most people do, but living on 35% of your income is no walk in the park.

I think the most common scenario for being able to retire really early is to get lucky with an investment. That could be a startup, a piece of property, or any number of things. We got lucky and bought our house at just the right time, and that is going to be a big enabler of our early retirement.

Like I said, I like the general theme of living off of less and saving more, but I don’t think we should make people feel like failures for having to work more than 10 years. It is important to be realistic and set people’s expectations accordingly.

The biggest hiccup in my retirement plan has been having children. Knowing in your mind how expensive they can be vs the reality of the money hemmoraging out of your bank account is a reality sandwich you just can’t anticipate.

I know many have successfully retired early with children, but it does make things more complicated.

I really like this way of looking at things. I built a grid myself but my figures look a little different. What real growth rate are you assuming for that grid? I’m assuming the withdrawal rate you’re using is the 3.5% you quoted below. Thanks!