Best Practices for the Inexperienced or Seasoned Investor Alike.

This is a guest post by Rob Pivnick, author of What All Kids (and adults too) Should Know About . . . Saving & Investing, Twitter: @RPivnick, www.whatallkids.com

| Nearly one-third of American adults have no savings at all for retirement. Almost one-half of all U.S. adults are not even thinking about saving for their retirement. And, believe it or not, a survey conducted by the Consumer Federation of America and the Financial Planning Association found that 21% of American adults actually think that winning the lottery is the most practical way for them to accumulate money for their retirement. Surely, however, you didn’t click on this blog to read that playing the lottery is not a sound long term strategy for retirement planning. |  |

The 2014 annual Wells Fargo Middle-Class Retirement study released in October revealed that 68% of all respondents felt that saving for retirement is harder than they anticipated. Below are six easy to follow rules that can form the basis of a smart long term investment plan to make investing easier.

Experienced investors likely know these “rules” already . . . but practicing them is harder than reading them. For millennials and other less experienced investors – follow these six tips to set yourself up for financial independence.

- START SAVING EARLY. LET COMPOUNDING WORK FOR YOU.

Albert Einstein was smart. He said “compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” Starting to save as early as possible is the easiest and best way to let your money work for you.

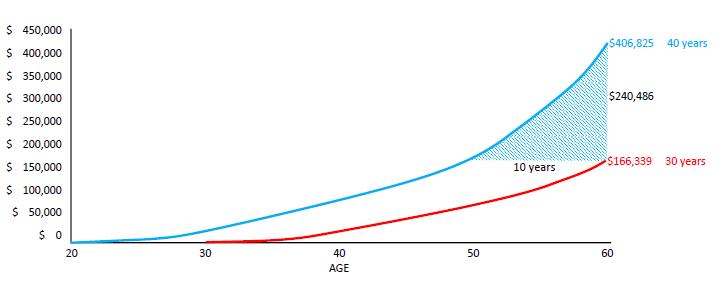

A chart helps you see why compounding makes such a difference. The below graphic shows two savers, both saving $100 per month at an annual average return of 8.5%. The blue line shows the saver who started when she was 20 years old. The red line shows someone who waited until she was 30. The ten year difference (which is only an additional $12,000 saved) results in over $240,000 more growth! So . . . start now.

- INVEST IN INDEXES; DON’T BE A FOOL AND TRY TO BEAT THE MARKET.

I’m not a great investor, I’m just average. And I’m comfortable with that. You should be too. It is better to be the market than try to beat the market. It isn’t very often in life that you don’t want to be the best, but when it comes to investing you should want to be average. Passive management, or indexing, is an investment approach in which the fund’s goal is to match the performance of the market as closely as possible, rather than try to beat it.

Over the long term it is impossible to consistently beat the market without taking on additional risk. The chart below shows how passive index funds beat actively managed funds over the five year period ended 2013. The percentages show how many actively managed funds beat the benchmark for their category.

| Anywhere from 65%-80% of funds cannot beat by the market. A dismally low 20%-35% of professionals beat the market year over year. In fact, over the 15 years ended 2011 a full 46% of actively managed funds closed due to poor performance. 7% of all actively managed funds failed every year. The professionals are not smarter than the market. Neither are you. |  |

Not only can active funds not beat the market, but they charge a full percentage point more on average than passive funds. And assuming active funds could match the market, the one percent fee equates to almost 12% of your returns assuming an 8.5% average annual return. Don’t give up that much for the same (if you’re lucky) return.

- DO NOT TRY TO TIME THE MARKET – YOU CAN’T. BUY AND HOLD IS THE BEST LONG TERM STRATEGY.

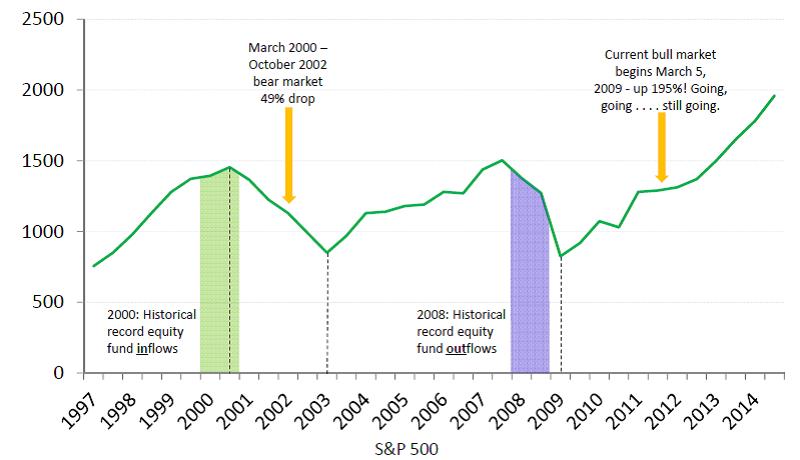

Depending on which research source used, the average investor’s annual return is anywhere between 3% and 5%. That’s compared to the historical average market return of 8.5%. Why? Because we are terrible at investing. We chase returns. We react to fear. We buy into the media hype. And we invest emotionally. Emotional investing causes most of us to buy high and sell low. In fact, the year 2000 saw a record inflow into domestic equity funds in history. Immediately following that the market dropped almost 50% (fueled by the dotcom bubble bursting). In 2008, the opposite occurred as a record was set for the most outflows of funds from domestic equity funds. What happened next? The market has been on an unprecedented climb since then, with returns reaching almost 200% from the market low. As of the date of this blog, it’s still climbing. And most investors missed out on that recovery.

- DO NOT CHASE RETURNS. THE MARKET ALWAYS REVERTS TO THE MEAN.

|

Of course you know that over the long haul, by definition, stock returns and markets will generate their historical average returns. Another way of saying this is that the market reverts to its mean and ultimately moves back towards its average return in the long term. Short term returns may vary, but the long term returns always revert to the average. |

Remember reversion to the mean. What’s hot today isn’t likely to be hot tomorrow. The stock market reverts to fundamental returns over the long run. Don’t follow the herd.One of Vanguard founder John C. “Jack” Bogle’s 10 Rules of Investing is as follows:

Emotional investing is a losing strategy. Investors fall into the be-a-part-of-the-crowd trap because social validation dictates that their investment decisions must be the “right” ones if others are doing the same thing. The media says buy, so most investors get in the market. And when everyone else is in a panic and selling, that’s what most people do. But you should stick to your long term plan. See # 3 above.

- MINIMIZE EXPENSES, INVEST IN LOW-COST INDEX FUNDS.

Every investor should know that past performance is no indication of future returns.What you might not know, however, is that the single most accurate predictor of future returns is low fees. That’s right. Studies have shown that focusing on low fees solely would result in better returns for investors. When looking at factors such as past performance, manager tenure, expense ratios and Morningstar ratings – expense ratios were the only reliable predictor of future performance. From Morningstar’s own Director of Fund Research Russel Kinnel: “If there’s anything in the whole world of mutual funds that you can take to the bank, it’s that expense ratios help you make a better decision. In every single time period and data point tested, low-cost funds beat high-cost funds. . . . Investors should make expense ratios a primary test in fund selection. They are still the most dependable predictor of performance.”

- DON’T PUT ALL YOUR EGGS IN ONE BASKET. STAY DIVERSIFIED AND FOLLOW A PLAN.

Diversifying won’t increase returns. But it does allow investors to lower risk without lowering the expected return. It can limit losses without sacrificing gains. It’s the only way to do that. Unfortunately, diversification won’t protect against the risk that the entire market goes south. But by spreading investments over a wide variety of sectors and asset classes in a smart way (those without high correlations to each other), the risk that any specific investment will fail is partially canceled by all other investments and overall risk is lowered. Investors can and should diversify among asset classes. And investors should also diversify within each type of asset (e.g., diversify among different sectors, geographical regions, market capitalization, industries, etc.).

| Invest in a mix of stocks, bonds, and other assets according to your individual goals and investment horizon. Don’t invest emotionally. Ignore the crowd. Stick to your long term plan and . . . please . . . turn off the financial news. |  |

Rob Pivnick is an investor, entrepreneur, attorney, residential real estate investor and financial literacy advocate. Rob has both a law degree and an M.B.A. from SMU in Dallas, TX. He is a member of the board of directors of the Texas affiliate of the national Council on Economic Education. Professionally, Rob is in-house counsel for Goldman, Sachs and Co. and specializes in finance and real estate.

Rob’s book, “What All Kids (and adults too) Should Know About Saving & Investing,” includes the topics above. It targets young adults/millennials with vocabulary words, fun facts, “Did you know?” sections, and 14 key takeaways. Statistics, charts and graphs from expert sources bolster the information. It aims to help students develop proper habits for saving and investing for long term. Not get rich quick. Chapters include budgeting, debt, setting goals, risk vs. reward, active v. passive strategies, diversification and more. Visit www.whatallkids.com for more information. Twitter: @RPivnick.

I never try my luck on lotto and never believe that this would secure my retirement. Like never in my entire life. I’ve started saving long term (retirement savings, housing, car, and others) at the age of 22, when I got myself a job which I consider very stable. Since then, I just take a portion of my salary for my long term savings. The idea of retirement occurred to me after graduation. It was really early for me. 😀

Jayson, kudos to you for starting early. Playing the lottery for fun isn’t the end of the world, I suppose (I don’t) but when people actually think that the lottery is a viable strategy for their retirement, that when we have problems. Global average savings rates are around 15%; the US is near the bottom at 4% only. That’s abysmal. Sounds like you place saving as a first line item of your budget, and you started early.

Rob

@rpivnick

http://www.whatallkids.com

I am amazed at how many people spend $20 or more each week to play lotto. If they would invest that money into index funds instead, it would be an almost guaranteed payoff down the road. I am too lazy to try and beat the market, so I really like your style of investing.

Great points all.

It helps to have investing goals as well. My wife and I have a series of cumulative goals, i.e. if we have $x at retirement we can do A but if we have $x we can do both A and B. There are five goals in all. It helps to keep us motivated knowing that we’ve reached a couple of goals but can make the others if we stretch a little.

I love the “pick 6” theme. I also LOVE index funds! I am almost fully invested in them through my IRA, my TSP and my wife’s 401k. They make investing for retirement simple and I love simple.

Congratulations, excelent tips and sure enough, as soon as we start before we will reap the rewards, very good article.

Congratulations, very good article.

i never try my luck on lotto and never believe that this would secure my retirement. Like never in my entire life

Very good article.

I play, but for fun, I’ve been working hard, I’ve been working on economics and financial education

I really liked your article

Rich content

http://debtblag.com/theyre-less-confident-retiring-comfortably-americans-buy-lottery-tickets-data/#comment-135550

My congratulations, an excellent article. Thank you for sharing with us!

Good article! Very nice!

I am very pleased with the information in this article, note 10!

Good article! Very nice!

My congratulations, an excellent article. Thank you for sharing with us!

Anyway stay up the nice high quality writing, it’s uncommon to look a nice blog like this one these days.. I would have never considered any of these if I didn’t come, Very good written article,I would like to thank you for the efforts you have made in writing this article.

i never try my luck on lotto and never believe that this would secure my retirement. Like never in my entire life

muito bom otimo conteudo gostei bastante

muito bom verdade seja dita

Congratulations, very good article.

NWM for me! I never win anything and was on pins and needles the day people started getting their emails. I’m so excited!! It will be my second 1/2. First one is Disney Princess on 2/24. 🙂

I am new and last couple of days i bear a huge loss can you please help me in the lottery system. Now i am stating to reading you all above mention tips. i hope it will best me in future.

it’s uncommon to look a nice blog like this one these days.. I would have never considered any of these if I didn’t come, Very good written article,I would like to thank you for the efforts you have made in writing this article. Crypto Currency news

I believe that it depends on each person, investing in business will always be good.

But in the lottery it is possible to have some change and maybe something big, it depends a lot on how you play.

But my congratulations for the post, very informative.

Very interesting and you have written the awesome story. The pic which you have mentioned the above column is also good and looks 100 years old 🙂 I really Loved this Article, very precise and to the point content. do you want to connect via email? Thanks by the way. Will keep visiting

one must be aware of the use of money, for it is not rare that millions of people have lost everything because they have not managed their fortura correctly.

Nice Article!! With his tips it will be possible to improve the lottery investment

Congratulations, very good article.